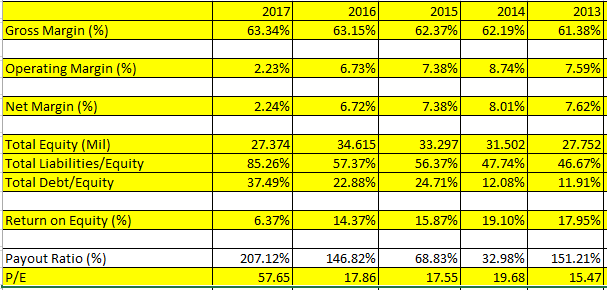

What attracts me to this counter is purely the huge discount to NAV. At almost 40% off using current price of $1.9 to NAV of $2.95. According to Peter Lynch 6 categories of stocks - this category is known as "Asset Play". Since valuation of property counters is usually measured by NAV.

Looking at the chart of NAV vs stock price. I like what I'm seeing here, NAV is growing while stock price is accumulating. This gives huge potential to the counter.

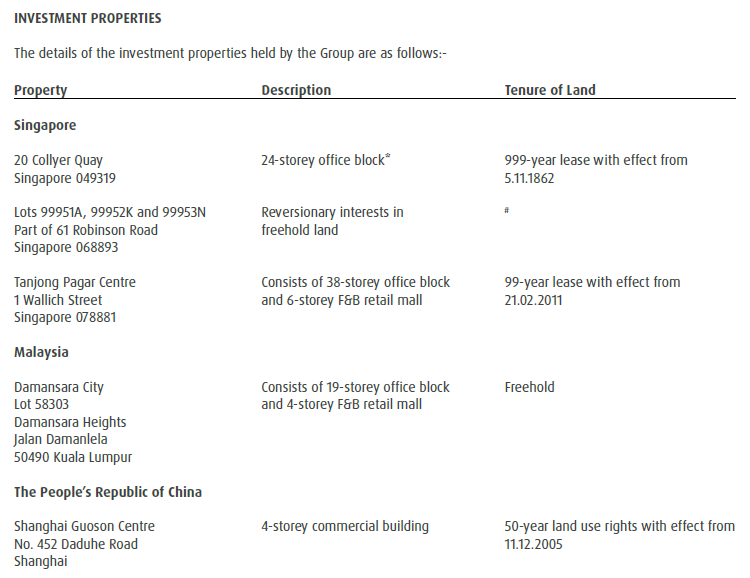

On another note, I like the fact that TPC (which completed in Oct 16) is providing the property developer counter with rental income, which goes in line with management "strategic goals of growing recurring income through investment properties to sustain future growth". Although the company huge revenue is still from sales of development properties, I would be expecting increasing opportunities by GL to invest more in investment properties to increase their recurring income.

On a last note, the counter has been giving out dividends quite consistently. Although the yield is about 2-3%. What's better than getting recurring income while waiting for the price to unlock. That might or might not happen in near future, patience is required.